|

| Thomas Jordan, Chairman of the Governing Board of the Swiss National Bank |

Negative interests rates are the shiny new thing that everyone wants to talk about. I hate to ruin a good plot line, but they're actually kind of boring; just conventional monetary policy except in negative rate space. Same old tool, different sign.

What about the tiering mechanisms that have been introduced by the Bank of Japan, Swiss National Bank, and Danmarks Nationalbank? Aren't they new? The SNB, for instance, provides an exemption threshold whereby any amount of deposits that a bank holds above a certain amount is charged -0.75% but everything within the exemption incurs no penalty. As for the Bank of Japan, it has three tiers: reserves up to a certain level (the 'basic balance') are allowed to earn 0.1%, the next tier earns 0%, and all remaining reserves above that are docked -0.1%.

But as Nick Rowe writes, negative rate tiers—which can be thought of as maximum allowed reserves—are simply the mirror image of minimum required reserves at positive rates. So tiering isn't an innovation, it's just the same old tool we learnt in Macro 101, except in reverse.

No, the novel tool that has been created is what I'm going to call a cash escape inhibitor.

Consider this. When central bank deposit rates are positive, banks will try to minimize storage of 0%-yielding banknotes by converting them into deposits at the central bank. When rates fall into negative territory, banks do the opposite; they try to maximize storage of 0% banknote storage. Nothing novel here, just mirror images.

But an asymmetry emerges. Central bankers don't care if banks minimize the storage of banknotes when rates are positive, but they do care about the maximization of paper storage at negative rates. After all, if banks escape from negative yielding central bank deposits into 0% yielding cash, this spells the end of monetary policy. Because once every bank holds only cash, the central bank has effectively lost its interest rate tool.

If you really want to find something innovative in the shift from positive to negative rate territory, it's the mechanism that central bankers have instituted to inhibit the combined threat of mass paper storage and monetary policy impotence. Designed by the Swiss and recently adopted by the Bank of Japan, these cash escape inhibitors have no counterpart in positive rate land.

The mechanics of cash escape inhibitors

Cash escape inhibitors delay the onset of mass paper storage by penalizing any bank that tries to replace their holdings of negative yielding central bank deposits with 0%-yielding cash. The best way to get a feel for how they work is through an example. Say a central bank has issued a total of $1000 in deposits, all of it held by banks. The central bank currently charges banks 0% on deposits. Let's assume that if banks choose to hold cash in their vaults they will face handling & storage costs of 0.9% a year.

Our central bank, which uses tiering, now reduces deposit rates from 0% to -1%. The first tier of deposits, say $700, is protected from negative rates, but the second tier of $300 is docked 1%, or $3 a year. Banks can improve their position by converting the entire second tier, the penalized portion of deposits, into cash. Each $100 worth of deposits that is swapped into cash results in cost savings of 10 cents since the $0.90 that banks will incur on storage & handling is an improvement over the $1 in negative interest they would otherwise have to pay. Banks will very rapidly withdraw all their tier-2 deposits, monetary impotence being the result.

To avoid this scenario, central banks can install a Swiss-style cash escape inhibitor. The way this mechanism works is that each additional deposit that banks convert into vault cash reduces the size of the first tier, or the shield, rather than the second tier, the exposed portion. So when rates are reduced to -1%, should banks try to evade this charge by converting $100 worth of deposits into vault cash they will only succeed in reducing the protected tier from $700 to $600, the second tier still containing the same $300 in penalized deposits. This evasion effort will only have made banks worse off. Not only will they still be paying $3 a year in negative interest but they will also be incurring an extra $0.90 in storage & handling ($100 more in vault cash x 0.9% storage costs).

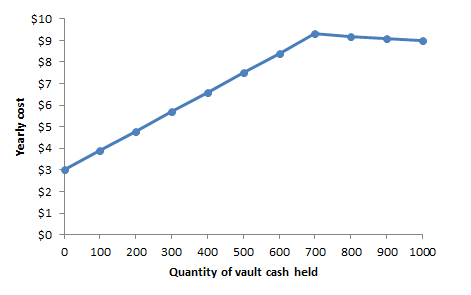

Continuing on, if the banks convert $200 worth of deposits into vault cash in order to avoid -1% interest rates, they end up worsening their position even more, accumulating $1.80 in storage & handling costs on top of $3.00 in interest. We can calculate the net loss that the inhibitor imposes on banks for each quantity of deposits converted into vault cash and plot it:

|

| The yearly cost of holding various quantities of cash at a -1% central bank deposit rate |

Notice that the graph is kinked. When a bank has replaced $700 in deposits with cash, additional cash withdrawals actually reduce its costs. This is because once the first tier, the $700 shield, is used up, the next deposit conversion reduces the second tier, the exposed portion, and thus absolves the bank of paying interest costs. And since interest costs are larger than storage costs, overall costs decline.

If banks go all-out and cash in the full $1000 in deposits, this allows them to completely avoid the negative rate penalty. However, as the chart above shows, storage & handling costs come out to $9 per year ($1000 x 0.9%), much more than the $3 banks would bear if they simply maintained their $300 position in -1% yielding deposits.

So at -1% deposit rates and with a fully armed inhibitor installed, banks will choose the left most point on the chart—100% exposure to deposits. Mass cash conversion and monetary policy sterility has been avoided.

How deep can rates go?

How powerful are these inhibitors? Specifically, how deep into negative rate territory can a central bank go before they start to be ineffective?

Let's say our central banker reduces deposit rates to -2%. Banks must now pay $6 a year in interest ($300 x 2%). If banks convert all $1000 in deposits into cash, they will have to bear $9 in storage and handling costs, a more expensive option than remaining in deposits. So even at -2% rates, the cash inhibitor mechanism performs its task admirably.

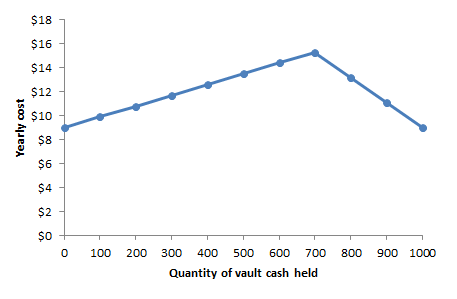

If the central bank ratchets rates down to -3%, banks will now be paying $9 a year in interest ($300 x 3%). If they convert all $1000 in deposits into cash, they'll have to pay $9 in storage & handling. So at -3%, bankers will be indifferent between staying invested in deposits or converting into cash. If rates go down just a bit more, say to -3.1%, interest costs are now $9.30. A tipping point is reached and cash will be the cheaper option. Mass cash storage ensues, the cash escape inhibitor having lost its effectiveness.

The chart below shows the costs faced by banks at various levels of cash holdings when rates fall to -3%. The extreme left and right options on the plot, $0 in cash or $1000, bear the same costs.

| |

|

So without an inhibitor, the tipping point for mass cash storage and monetary policy impotence lies at -0.9%, the cost of storing & handling cash. With an inhibitor installed the tipping point is reduced to -3.1%. The lesson being that cash escape inhibitors allow for extremely negative interest rates, but they do run into a limit.

The exact location of the tipping point is sensitive to various assumptions. In deriving a -3.1% escape point, I've used what I think is a reasonable 0.9% a year in storage and handling costs. But let's assume these costs are lower, say just 0.75%. This shifts the cash tipping point to around -2.5%. If costs are only 0.5%, the tipping point rises to around -1.7%.

This is where the size of note denominations is important. The Swiss issue the 1000 franc note, one of the largest denomination notes in the world, which means that Swiss cash storage costs are likely lower than in other countries. As such, the Swiss tipping point is closer to zero then in countries like the Japan or the U.S.. One way to push the tipping point further into negative terriotry would be a policy of embargoing the largest note. The central bank, say the SNB, stops printing new copies of its largest value note, the 1000 fr. Banks would no longer be able to flee into anything other than small value notes, raising their storage and handling costs and impinging on the profitability of mass cash storage.

Good old fashioned financial innovation will counterbalance the authorities attempts to drag the tipping point deeper. Cecchetti & Shoenholtz, for instance, have hypothesized that in negative rate land, a new type of intermediary could emerge that provides 'cash reserve accounts.' These specialists in cash storage would compete to reduce the costs of keeping cash, pushing the tipping point back up to zero.

The tipping point is also sensitive to the size of the first tier, or the shield. I've assumed that the central bank protects 70% of deposits from the negative deposit rate. The larger the exempted tier the bigger the subsidy central banks are providing banks. It is less advantageous for a bank to move into cash when the subsidy forgone is a large one. So a central bank can cut deeper into negative territory the larger the subsidy. For instance, using my initial assumptions, if the central bank protects 80% of deposits, then it can cut its deposit rate to -4.6% before mass paper storage ensues.

Removing the tipping point?

There are ways to modify these Swiss-designed cash escape inhibitors to remove the tipping point altogether. The way the SNB and BoJ have currently set things up, banks that try to escape negative rates only face onerous penalties on cash conversions as long as the first tier, the shield, has not been entirely drawn down. Any conversion after the first tier has been used up is profitable for a bank. That's why the charts above are kinked at $700.

If a central bank were to penalize cumulative cash withdrawals (rather than cash withdrawals up to a fixed ceiling) then it will have succeeded in snipping away the tipping point. This is an idea that Miles Kimball has written about here. One way to implement this would be to require that the tier 1 exemption, the shield, go negative as deposits continue to be converted into cash, imposing an obligation on banks to pay interest. The SNB doesn't currently allow this; it sets a lower limit to its exemption threshold of 10 million francs. But if it were to remove this lower limit, then it would have also removed the tipping point.

What about retail deposits?

You may have noticed that I've left retail depositors out of this story. That's because the current generation of cash escape inhibitors is designed to prevent banks from storing cash, not the public.

As central bank deposit rates fall ever deeper into negative territory, any failure to pass these rates on to retail depositors means that bank margins will steadily contract. If banks do start to pass them on, at some point the penalties may get so onerous that a run develops as retail depositors start to cash out of deposits. The entire banking industry could cease to exist.

To get around this, the FT's Martin Sandbu suggests that banks could simply install cash escape inhibitors of their own. Miles Kimball weighs in, noting that banks may start applying a fee on withdrawals, although his preferred solution is a re-deposit fee managed by the central bank. Either option would allow banks to preserve their margins by passing negative rates on to their customers.

Even if banks don't adopt cash escape inhibitors of their own, I'm not too worried about retail deposit flight in the face of negative central bank deposit rates of -3% or so. The deeper into negative rate territory a central bank progresses, the larger the subsidy it provides to banks via its first tier, the shield. This shielding can in turn be transferred by a bank to its retail customers in the form of artificially slow-to-decline deposit rates. So even as a central bank reduces its deposit rate to -3% or so, banks might never need to reduce retail deposit rates below -0.5%. Given that cash handling & storage costs for retail depositors are probably about the same as institutional depositors, banks that set a -0.5% retail deposit rate probably needn't fear mass cash conversions.

So there you have it. Central banks with cash escape inhibitors can get pretty far into negative rate land, maybe 3% or so. And with a few modifications they might be able to go even lower.

Good post.

ReplyDelete1. Cash escape bans are like banning 100% reserve banking. Central banks refuse to nationalise the asset side of banks' balance sheets.

2. If central banks can measure banks' cash holdings, they could pay negative interest on those cash holdings.

3. I had a third thing to say, but it's slipped my mind.

3. Maybe this was it: 100% reserve banking does not make monetary policy impotent.

DeleteDecided to do a quickie post on this: http://worthwhile.typepad.com/worthwhile_canadian_initi/2016/02/some-thoughts-on-banning-100-reserve-banking.html

DeleteNice post.

ReplyDeleteBut there is a massive chunk of balance sheet analysis that I don't believe you've tackled directly in your series of posts related to this issue.

That is - the order of magnitude relationship between the size of the reserve position that is in place (for whatever reason - QE or not) and the size of bank liabilities that have the same liquidity risk sensitivity as currency. I.e. a sizable component of bank funding consists of term liabilities that are effectively protected against the type of near term redemption that poses the risk of conversion into currency. This is also a fundamental aspect of commercial bank liquidity management. All sorts of additional sensitivity analysis opens up because of this.

To eliminate cash withdrawal is a terrible practical mistake. It badly confuses the whole issue.

ReplyDeleteWhat central banks should say instead is that additional voluntary withdrawals by either the public or the banking system will be treated in the future as if they were permanent injections of zero yielding base money (that is remain as vault or publicly held cash or be treated as required reserves in the event rates need to go above zero in the future). It is shocking to me that people dont understand this. But of course once you see this perspective, the whole need for negative rates becomes much less pressing. Although I personally dont mind the idea of a modestly negative policy rate in order to help in the calibration of how much Base Money increase can be made permanent and nonetheless consistent with long-term objectives: I.e. price level targets, ngdp targets, inflation targets, currency pegs, etc...

There is something massively wrong with this article! reserves are defined as deposits at the FED AND cash held at the bank. So there is no way a bank can reduce its reserves by holding cash, since that cash is still counted as reserves....big error in the article

ReplyDeleteAnother problem is that if the bank reduced its reserves by $300 it would pay -1% on 300 of the remaining $700. This would be out of line with a bank which started with $700. Banks would have to make sure they never held excess reserves at the Central Bank. Better to use the shadow banks for this.

ReplyDeleteI think that you are overestimating the expenses of storing cash. The storage costs should be pretty much fixed, and only slightly related to the amount of banknotes stored.

ReplyDeleteI'm not so sure that all that has any sense. We re talking about negative interest rates, which imply a negative yield curve. Is that possible? I'm affraid that there is no simetry between a positive yields curve and a negative one. This last is impossible, because risk will never be negative. So, all these exercises of inhibiting the swap from reserve toward cash has an obvious limit. We are going to dangerous and unexplored territory.

ReplyDeleteBeside that, I see some consequences for basic Liberty, a the right of store asset as anyone will. All you propose is a confiscation of this basic individual liberty. What is the next?

ReplyDelete